by

by Sometimes in life, there are those “aha” moments that make you wonder if you’re living in a different universe. We’ve mentioned before that we were looking for financing for our home construction project. The goal was simple: avoid selling investments and getting hit with a massive tax bill in one year. But here’s the thing: when your income comes from investments and retirement accounts instead of a regular paycheck, traditional financing can be a real headache.

When Traditional Options Hit a Wall

Despite having excellent credit scores and substantial investments we could turn into income, conventional home equity loans were off the table. Banks have a funny way of looking at income—if it doesn’t come in the form of a steady paycheck, they tend to get nervous. So we tried that route, and it didn’t work.

That led us to explore asset-based loans. Before our design was finalized and we gathered estimates, we started shopping around for a loan to fund at least 50% of the construction, which at the time would’ve been around $200,000.

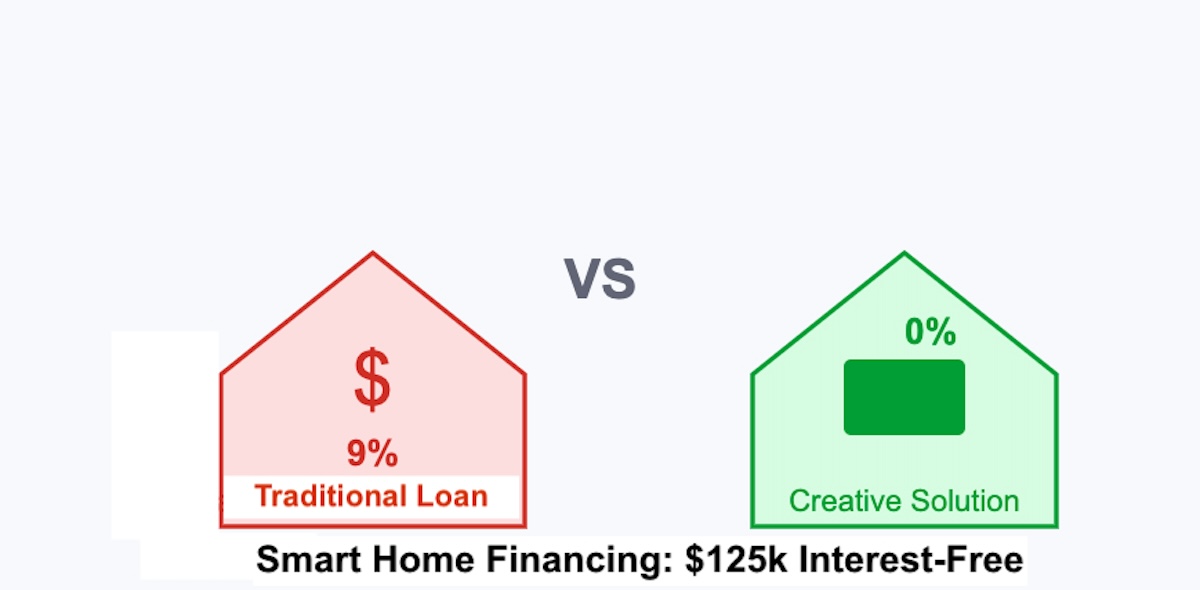

One lender offered what seemed like a solution, but the numbers told a different story. Their asset-based cash-out refinance proposal was eye-opening, but not in a good way. They wanted us to borrow $320,000 to receive $182,093 in cash, with a steep 9% interest rate and hefty closing costs of $18,300. This would also mean refinancing our current mortgage (under $116,500 at 3%) into a 9% mortgage.

Over just two years—our estimated build completion time—the total cost would hit $68,910. That includes $13,980 in additional interest on our existing mortgage amount, plus $36,630 in interest on the new borrowed amount, and those substantial closing costs. After accounting for all expenses and mortgage payments, we’d need to pay $50,610 extra just to maintain the mortgage payments. In the end, we’d only have $131,483 available for actual construction, despite taking on $320,000 in debt.

To put this in perspective, if we could find alternative financing at 6% interest, the total cost for borrowing the same amount would be just $21,851—less than a third of the cost of the asset-based loan. The difference was staggering.

Asset-Based Loan Proposal

Total loan amount: $320,000 at 9% interest rate

Existing mortgage refinance: $116,500 from 3% to 9%

New Interest Costs (2 Years)

Existing Mortgage Impact

Closing Costs

Extra Mortgage Payments

Final Impact

Enter Plan C: A Creative Solution

We started looking at financial institutions offering no-interest or very low-interest financing for materials and appliances. But the real breakthrough came from an unexpected direction—our years of credit card travel hacking experience.

Here’s something we’ve learned over the years: keeping one no-annual-fee credit card open with each major bank can be incredibly valuable. When we’d open a card for travel rewards, we’d transfer the available credit to our keeper card before closing it. Over time, this strategy helped us build up significant credit lines.

Through years of this practice, we had accumulated over $100,000 in available credit across four cards that we have open with just one bank. Then we discovered something interesting: new cards offering no interest for 18 months on purchases. That’s when the lightbulb went on.

We approached the bank about opening new cards with those favorable terms. Initially, they only offered $5,000 limits—barely enough for a couple of construction purchases. But here’s where our previous credit building paid off: we asked to transfer most of our existing credit lines to the new no-interest cards, leaving just about $1,000 on each original card.

The bank representatives found it a bit unusual that someone would want to transfer such large credit lines, but they processed the changes. We repeated this process with my wife’s cards and then opened another card with a different bank offering $25,000 with no interest for 18 months and 2% cash back! So we’re even getting paid to take this offer!

The Power of Creative Thinking

Through this strategy, we secured $125,000 in no-interest financing for 18 months—with zero upfront fees. This allows us to delay selling investments that could bump us into a higher tax bracket during the construction year. We’re effectively saving 10% in taxes, plus our funds continue earning dividends.

Asset-Based Loan

- $131,483 Available Cash

- 9% Interest Rate

- $18,300 Closing Costs

- $68,910 Total Cost (2 years)

Creative Solution

- $125,000 Available Credit

- 0% Interest Rate

- No Closing Costs

- $0 Total Cost (18 Months)

Now, I want to be crystal clear: this strategy isn’t about taking on credit card debt. I strongly advise against carrying credit card balances if you can’t pay them off each month; those interest rates are brutal. This approach only makes sense if you have the means to pay the bill when it’s due and can maintain an organized tracking system for due dates and payments.

What started as a challenge turned into an opportunity to think differently about financing. Sometimes the best solutions come from unexpected places—in our case, years of travel hacking gave us the knowledge and credit profile to make this work.