by

by Hola, mi gente! Welcome to our much-anticipated One Life to Live update. We’ve been quiet for a while, but for good reason—we’ve been busy preparing for a major life change. And now, we’re thrilled to announce:

We Retired!

Yes, you read that right. We retired from our corporate jobs at the ages of 33 and 44! This is what we’ve been working towards on our FIRE (Financial Independence, Retire Early) journey, and it’s finally happened. There’s no going back now—we quit our jobs, and everything unfolded so quickly we barely had time to process it.

We were certain of our decision, though, so there wasn’t much to ponder. In fact, most of our peers learned about our FIRE plans before we retired, thanks to our feature on MarketWatch in April. Welcome to our new readers from our work network!

I returned from paternity leave on July 1st and gave a three-week notice. The next day, Tatiana gave her notice, and it was epic! We’ll share more details in a future post, but we couldn’t wait to share this big news with you.

Life Changes and New Adventures

Retiring wasn’t our only big change. We also:

- Moved to our paid-off rental property

- Started renovating our new home

- Began planning for a snowbird lifestyle

We didn’t travel much in the first half of the year, aside from a trip to Florida in January and visiting Providence, RI in June. Why take limited vacations when a permanent vacation was right around the corner?

Now that we’re retired, we’re excited to explore more. We’re currently writing this from Europe, where we’ve been for three weeks!

Financial Update: Spending, Portfolio Performance, and Net Worth

As always, we want to be transparent about our finances. Here’s a breakdown of our spending for the first half of 2019:

| Category | 1st Half of 2019 Amount |

|---|---|

| Home | $27,675 |

| Kids | $6,131 |

| Food & Dining | $5,670 |

| Gifts & Donations | $1,935 |

| Travel | $1,420 |

| Bills & Utilities | $1,335 |

| Auto & Transport | $1,223 |

| Health & Fitness | $949 |

| Other | $1,170 |

| Total | $47,508 |

Our total spending for the first half of 2019 was $47,508. This is higher than usual due to home improvements ($16,283) and some one-time expenses related to our transition to early retirement. We don’t expect to spend as much in the future.

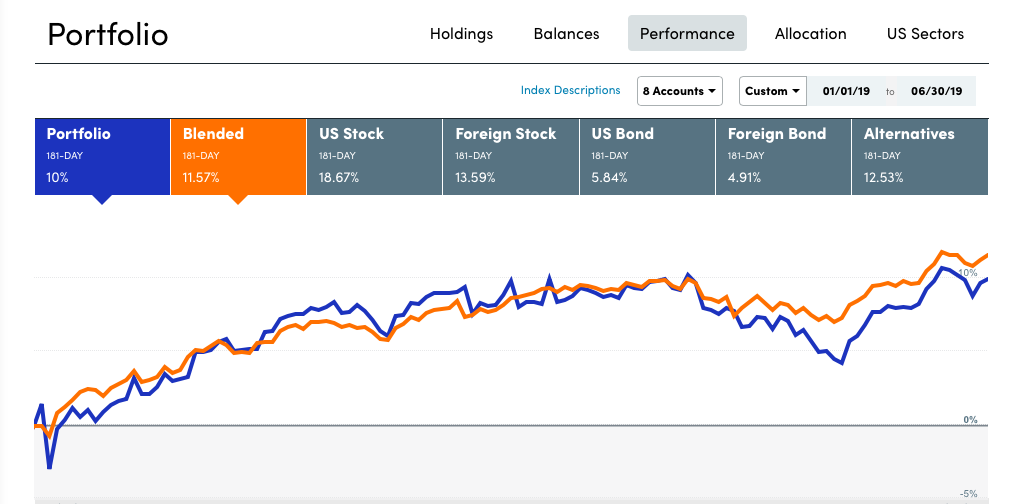

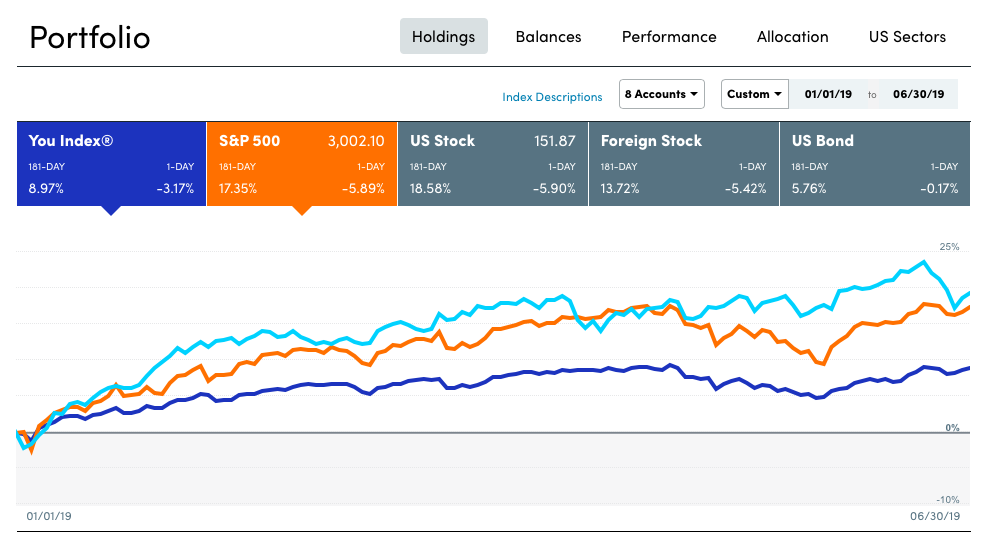

Portfolio Performance

Our Freedom Fund portfolio returned 10% for the first half of the year. This is about 8-9% lower than the S&P 500, which aligns with our more conservative 75% stocks / 25% bonds allocation. Remember, we’re retired now—we need that fixed income!

Our REIT holdings have been particularly strong, returning 19.29% from January to June. They currently make up 7.6% of our portfolio, and we aim to increase this to 10%.

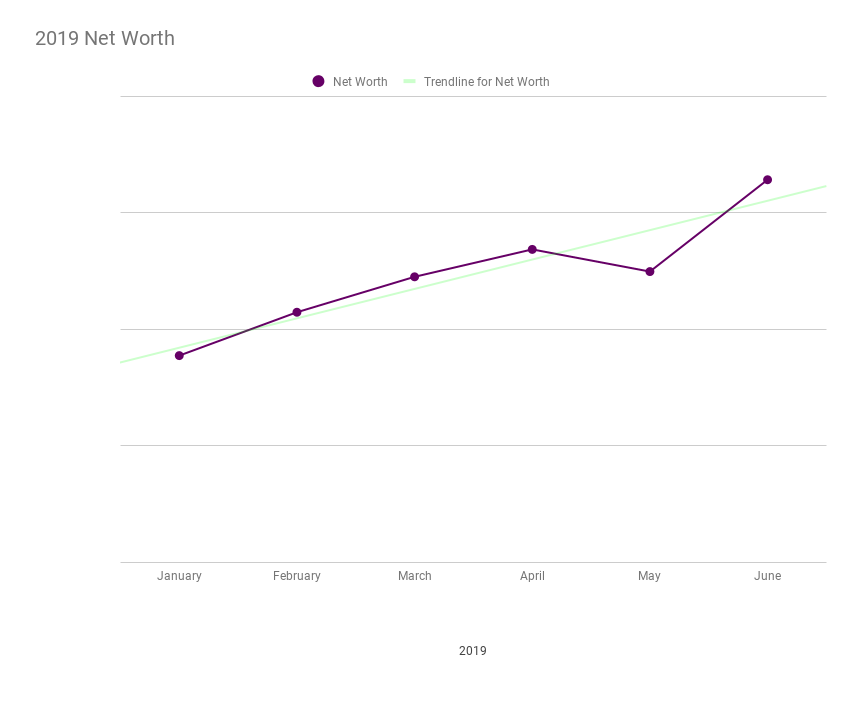

Net Worth Update

We’re happy to report that our net worth has surpassed our original FI (Financial Independence) target. However, we’re proceeding with caution for several reasons:

- We’re retiring at the end of a long bull market

- Healthcare costs in the U.S. remain a concern

- We’re planning for a potentially 60-year retirement

To address these concerns, we’re implementing several strategies:

- Planning to withdraw less than 4% annually

- Maintaining flexibility in our living situation

- Exploring international healthcare options

Looking Ahead

We’re still establishing our early retirement routine, but we’re loving the freedom from the 9-to-5 grind. Most importantly, we’re cherishing every moment with our little one, witnessing all her firsts—that alone makes it all worthwhile.

This is all so exciting! Congratulations!! With a such a young kid, it feels like you pulled the plug at the right time for the right reasons. I couldn’t be happier for you – or more jealous!

Hola!!! 🙂

It definitely feels like the right moment to do this. We’ll be around her when she needs us the most and wants to be around us. 😉

Thank you for stopping by!

Congratulations!

I’d love to know more about the numbers and how much your investment portfolio spits out to cover your expenses. We found with having a kid that our expenses are going on, so we are actively trying to boost our passive retirement portfolio by another $50,000 a year. But I don’t think we’ll get there for another three years.

Have your phone you needed to have more or make more once your child was born?

Sam

Thanks Sam!

Our entire portfolio’s income, including the funds to buy a house that are in money market account, was $40,568 last year. We own our current home outright. It was a rental property, but we decided to move in for now since we still need to decide where we want to live by the time our little one needs to attend school.

We were aiming for a spending budget of $40k a year with a paid-off home. Given our previous dividend income I feel strongly about being able to live off the dividends without tapping into investment gains.

We’re in the process of analyzing how much we should keep in the house fund given that a) we don’t see ourselves moving within the next 3 years and b) we have about $120k of home equity that we can use towards the future purchase. This gives us more flexibility with cash in early retirement as most of our money is in retirement accounts that can be touched until traditional retirement age.

As far as kid spending. It hasn’t been that bad for us. We expected to pay for a babysitter this year but now we’re home and don’t need it. Baby now eats mostly from what we cook and she gets lots of present from friends and family so we don’t spend much on her.

We planned our early retirement with a couple of kids in mind, and we also plan to live in areas with a lower cost of living than west coast.

Thanks for commenting, buddy!

Cool! Everything should work out!

Jubilado!

Jubilation!

A sincere congratulations to both of you. Enjoy!

-PoF

Thank you, sir! Congratulations to you as well on your early retirement and new home purchase. We might cross path on our travels.

Great Post 🙂

Financial goal I accomplished this year: downpayment for my first apartment and a savings I am proud of! With the help of two(and third is still a baby) very helpful people

Thanks Jessya! I’m glad you were able to meet those goals! 🙂 I can’t wait to see your story continue to unfold.