by

by Welcome to our quarterly recap of One Life To Live, where we share how financial independence is fueling our journey to true happiness. This quarter has been particularly exciting as we welcomed a new member to our family!

New Beginnings: From a Duo to a Trio

Our household has grown from two to three! We’re thrilled to announce the arrival of our daughter, Yuna. Born slightly under six pounds, she’s already weighing 12 pounds at 10 weeks. As Tatiana lovingly calls them, she’s got all the baby rolls (or “Michelin Man” rolls).

The first trimester with Yuna has been all-consuming, but incredibly rewarding. Her smiles, even during middle-of-the-night diaper changes, make all the tiredness melt away.

Balancing Work and Family

For me, it’s been challenging to leave for work each day. I’m away for just a few hours, and I already want to be back home with my family. This experience has reinforced our commitment to our FIRE plan. Knowing that corporate work is temporary and that we’re months away from retirement keeps us motivated.

Nesting and Cooking at Home

With Yuna in our lives, our lifestyle has shifted. We’re eating out less and cooking more at home. This change has not only been cost-effective but also allows us to use better ingredients and control what goes into our meals.

Some of our favorite homemade dishes this quarter included:

- Blueberry pancakes with organic turkey bacon

- Dominican-style beans with rice, chicken or fish, green salad, and avocado

Financial Update: Q3 2018

Bare-bones Expenses

Our basic expenses for Q3 2018 totaled $6,227.12, bringing our year-to-date total to $13,186.17.

| Category | Quarter Amount | YTD Amount |

|---|---|---|

| Auto & Transportation | $945.69 | $2,056.28 |

| Bills & Utilities | $565.80 | $1,585.90 |

| Groceries | $2,280.80 | $5,020.20 |

| Home Supplies | $179.05 | $596.57 |

| Net Rent | $2,255.78 | $3,927.22 |

| Total | $6,227.12 | $13,186.17 |

Our grocery spending has increased due to eating out less and buying high-quality ingredients for home-cooked meals. We’re focusing on convenience and quality over bargain hunting for now, but plan to optimize this in retirement.

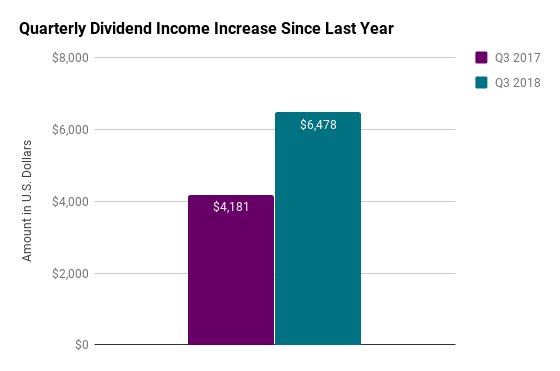

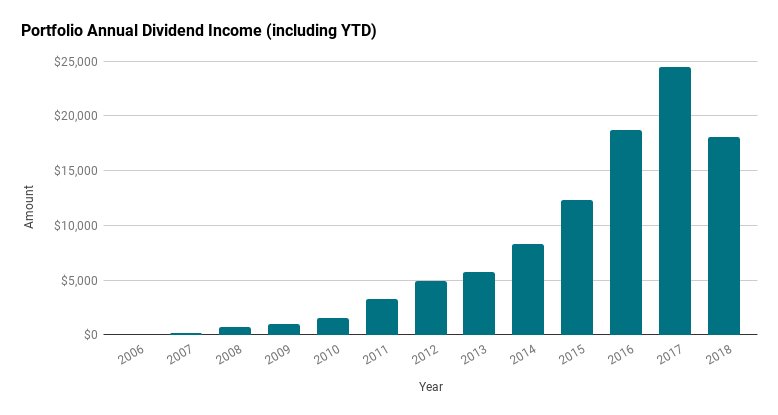

Passive Income

Our dividend income continues to grow, reaching $6,478 this quarter—a 54.9% increase from last year. We’re on track to surpass $30,000 in dividends this year.

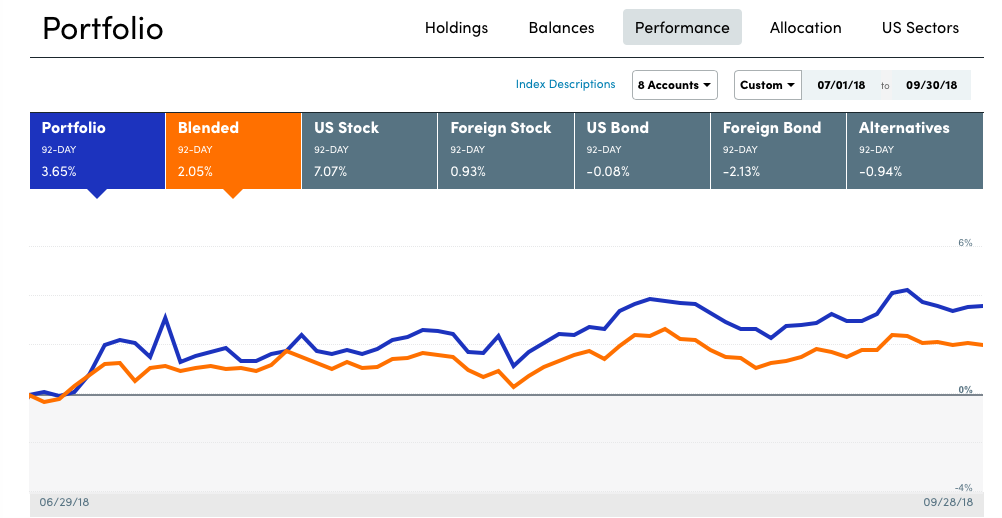

Portfolio Performance

Our Freedom Fund Portfolio returned 3.65% for the quarter, outperforming our blended benchmark. Year-to-date, our portfolio is up 3.46%. While not as high as pure stock returns, we’re comfortable with this performance given our 75/25 stock/bond allocation as we approach retirement.

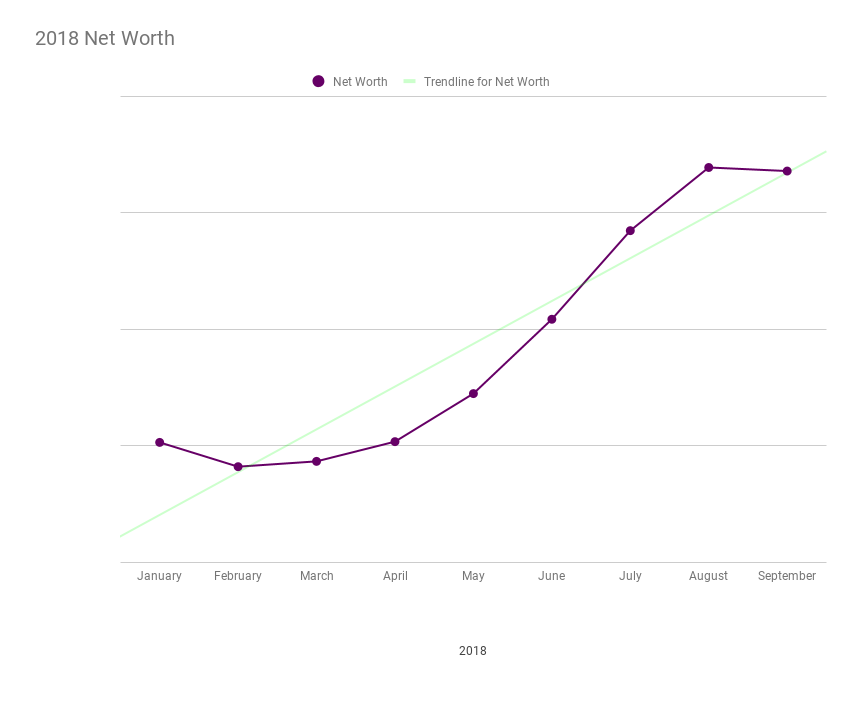

Net Worth Update

Our net worth continues to trend upward, staying above our projected trend line. We’ve maxed out our 401(k)s, Roths, and house fund, and continue to invest for our retirement needs.

Looking Ahead: The Road to Retirement

We’re just months away from early retirement! Before that, we’re preparing for our last winter in PA and planning a 5-week trip to Florida. This trip will allow us to escape the cold, spend time with family, and scout potential areas for our future home.

Our retirement fund targets are on track, with some accounts already exceeding our goals. We’re focusing our efforts on building our brokerage account for the remainder of the year.

Reflections on Parenthood and FIRE

Becoming parents to Yuna has reinforced the value of our FIRE journey. The ability to spend more time with her and have the flexibility to prioritize family over work is priceless. While our expenses have increased in some areas, we’ve found that the joy of parenthood far outweighs any financial adjustments we’ve had to make.

We’re excited about the next chapter of our lives and look forward to sharing our continued journey with you. Have you experienced significant life changes on your path to financial independence? We’d love to hear your stories in the comments below!

Stay tuned for our next update, where we hope to be writing from sunny Florida with Yuna enjoying her first solid foods. Until then, keep living your one life to the fullest!