by

by Welcome to part two of our Early Retirement Projections Series! In part one, we estimated our expenses in early retirement. Now, let’s dig deeper into our withdrawal strategy and how we plan to cover our retirement expenses. This isn’t just about crunching numbers; it’s about creating a sustainable lifestyle that balances our financial needs with our dreams for the future.

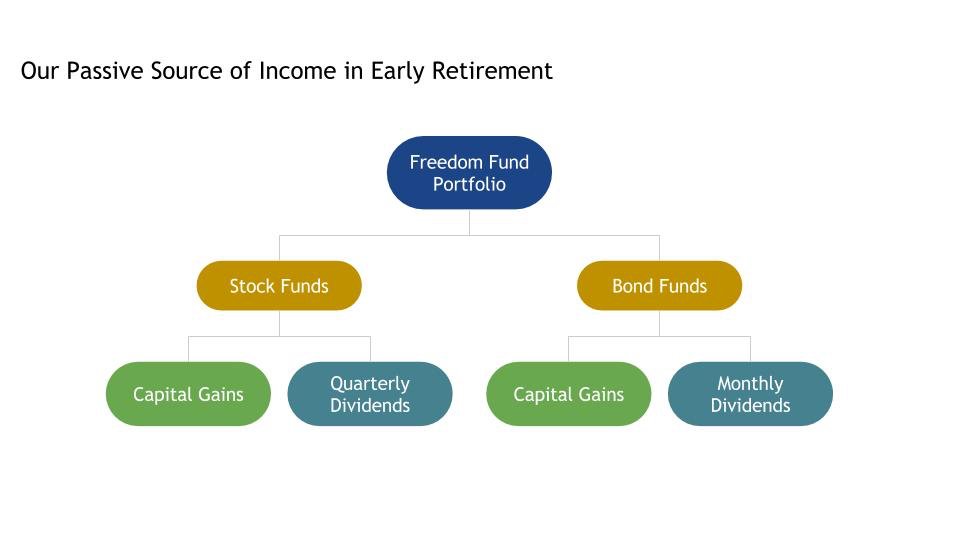

Our Freedom Fund: The Key to Financial Independence

Our Freedom Fund Portfolio will be our main source of income in early retirement. This carefully curated collection of investments will provide us with quarterly dividends from stock funds and monthly dividends from bond funds. It’s not just a nest egg; it’s our ticket to freedom!

Breaking Down the Freedom Fund

Our portfolio consists of:

- 75% stocks (primarily low-cost index funds tracking the total US and international markets)

- 25% bonds (a mix of government and high-quality corporate bonds)

This allocation provides a balance between growth potential and stability. We’ve chosen this mix based on extensive research and our personal risk tolerance. Remember, your ideal allocation may differ based on your unique circumstances and goals.

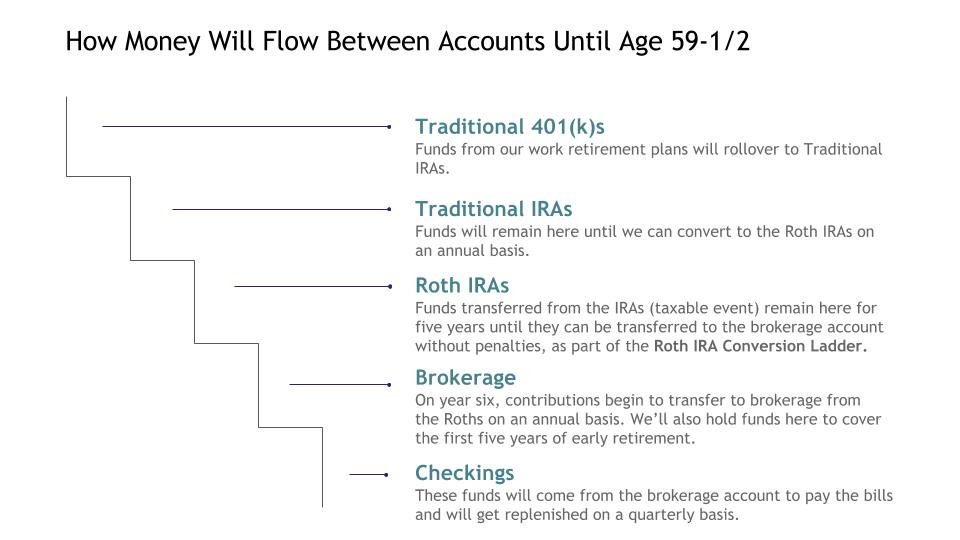

Accessing Our Funds: The Roth IRA Conversion Ladder

Since we’re younger than 59-1/2, we need a smart strategy to access our retirement funds without penalties. Enter the Roth IRA Conversion Ladder! This flexible method allows us to transfer money from our 401(k)s to IRAs, and then to Roth IRAs. After a five-year waiting period, we can access these funds tax-free and penalty-free.

How the Roth IRA Conversion Ladder Works

- Convert a portion of our traditional IRA to a Roth IRA each year.

- Pay taxes on the converted amount in the year of conversion.

- Wait five years.

- Withdraw the converted amount tax-free and penalty-free.

By repeating this process annually, we create a “ladder” of accessible funds. It’s like building a staircase to our financial future!

For the first five years of early retirement, we’ll rely on our brokerage account. It’s like a financial bridge to our future!

Our Withdrawal Strategy: Flexibility is Key

Most retirement strategies are based on the 4% rule, but we’re taking a more dynamic approach. Our withdrawal strategy is built on four pillars:

- Flexibility: We’ll adjust our spending based on market conditions. Down market? Maybe we’ll swap that European vacation for a Latin American adventure! This flexibility extends to our budget categories. We’ve identified areas where we can easily cut back (like entertainment and dining out) and areas that are more fixed (like housing and healthcare).

- Simplicity: We’ll review our finances quarterly, coinciding with dividend payments and portfolio statements. This approach allows us to stay on top of our finances without becoming obsessed with daily market fluctuations. Each quarter, we’ll:

- Review our spending from the previous quarter

- Assess our investment performance

- Make any necessary adjustments to our withdrawal amount

- Plan for the upcoming quarter

- Responsiveness: Our withdrawals will be sensitive to market performance. Bad quarter? We’ll tighten our belts a bit. Here’s how we’ll adjust:

- If quarterly returns are negative, we’ll withdraw less than our target amount and dip into our cash reserves.

- If returns are positive but below average, we’ll withdraw our target amount.

- If returns are above average, we’ll withdraw up to 4% and use any excess to replenish our cash reserves or fund larger discretionary expenses.

- Limited Risk: By withdrawing less during market downturns, we’ll mitigate the sequence of return risk. This risk is particularly important in the early years of retirement, when a series of poor returns can significantly impact long-term portfolio sustainability.

The Power of Flexibility

Our flexible approach allows us to adapt to changing market conditions and personal circumstances. For example, if we experience a prolonged market downturn, we have several levers we can pull:

- Reduce discretionary spending

- Tap into our cash reserves

- Consider part-time work or side hustles

- Delay major purchases or travel plans

By remaining adaptable, we increase our chances of long-term success and reduce the stress associated with rigid withdrawal rules.

The Numbers: How Much Will We Withdraw?

We estimate withdrawing between $40,000 to $42,000 annually in early retirement, based on average market returns. This should comfortably cover our projected budget of $38,000, not including health insurance and donations.

Breaking Down Our Budget

Here’s a rough breakdown of our anticipated annual expenses:

- Housing (including utilities): $12,000

- Food (groceries and dining out): $6,000

- Transportation: $3,000

- Healthcare (estimated): $8,000

- Entertainment and Travel: $6,000

- Miscellaneous: $3,000

This budget reflects our values and priorities. We’ve chosen to allocate more to travel and experiences while keeping our housing costs relatively low. Your budget may look different based on your lifestyle preferences and location.

Putting Our Strategy to the Test

Using the Crowdsourced FIRE Simulator, we ran a 60-year retirement scenario with a 75% stocks / 25% bonds portfolio. The results? An 86% success rate without any additional income or adjustments. Add in estimated Social Security benefits, and we’re looking at a 100% success rate!

Interpreting the Results

While these simulations are encouraging, it’s important to remember that they’re based on historical data and assumptions about the future. We’re not relying solely on these projections. Instead, we’re using them as one tool in our planning toolkit, alongside our flexible withdrawal strategy and willingness to adapt.

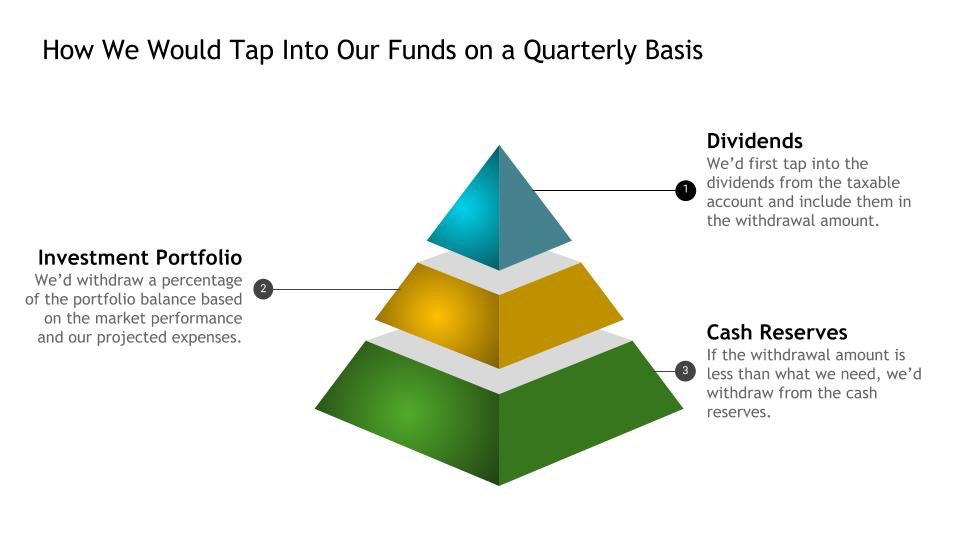

Our Quarterly Game Plan

Every quarter, we’ll:

- Add up dividend income

- Project expenses for the next quarter

- Withdraw what we need from the portfolio

During market downturns, we’ll tap into our one-year cash reserve to cushion the blow. In good quarters, we’ll withdraw up to 4% and replenish our cash reserve.

The Importance of Cash Reserves

Our one-year cash reserve serves several purposes:

- Provides a buffer during market downturns

- Reduces the need to sell investments at inopportune times

- Offers peace of mind and financial stability

We’ll aim to maintain this reserve through a combination of dividends, portfolio withdrawals, and potentially part-time work if necessary.

Embracing an Abundance Mindset

While our portfolio is our primary tool for financial independence, it’s not our only potential source of income. We’re open to earning more if we choose, but our main goal is happiness and life satisfaction.

The Power of Financial Independence

This journey isn’t just about money–it’s about freedom. Freedom to spend our time as we choose, to pursue our passions, and yes, to watch the sunset any day of the week!

What Financial Independence Means to Us

For us, financial independence represents:

- The ability to prioritize relationships and personal growth

- The opportunity to travel extensively and immerse ourselves in new cultures

- The time to volunteer and give back to our community

- The freedom to say “yes” to exciting opportunities without worrying about a paycheck